The UK is the leading Western hub for Islamic finance, sitting at the heart of global sukuk markets and international capital flows. London alone accounts for around 40% of hard-currency sukuk issuance worldwide, underpinned by the London Stock Exchange and a mature ecosystem spanning banking, asset management, professional services and fintech.

The UK Islamic finance sector is now worth more than £6 billion and is on track to double in size over the coming years. There are more than 50 Islamic fintech firms operating in the UK, including a fully digital Islamic bank, alongside growing activity across funds, capital markets and cross-border investment. Add in demographic change, rising interest in ethical and ESG-aligned finance and government initiatives such as Sharia-compliant student loans, and the sector is no longer talking to the same audience it was a decade ago.

That growth means Islamic finance providers in the UK are increasingly judged alongside mainstream financial institutions, under the same regulatory, reputational and media spotlight. And as activity spreads beyond London into the UK regions, that spotlight only gets brighter.

Against this backdrop, public relations and marketing can play a role in supporting Islamic finance providers at every stage of their UK journey, whether entering the market, scaling operations, competing for institutional capital or broadening appeal beyond core audiences.

Islamic finance’s history in the UK

Islamic finance has actually been part of the financial landscape for more than forty years.

It first arrived in the early 1980s with murabaha-based transactions, followed by the launch of the UK’s first Islamic bank, Al Baraka International, in 1982. From there, growth was steady, expanding across trade finance, leasing and project finance, supported by increasing expertise in law, accounting and advisory services.

In the early 2000s there was a shift; the UK Government began actively adapting regulation and tax treatment so that Islamic and conventional finance structures with equivalent outcomes were treated the same. This removed practical barriers and sent a clear signal that Islamic finance was now a recognised part of the UK financial system.

Capital markets followed. Sukuk listings began in London in 2007, and in 2014 the UK became the first Western government to issue a sovereign sukuk, heavily oversubscribed and widely seen as a statement of intent. Alongside banking and capital markets, the UK built strength in Islamic funds, insurance and the supporting professions, underpinned by a growing base of academic and professional education.

Today, the UK is home to multiple fully Sharia-compliant banks, more than twenty institutions offering Islamic finance services and a professional ecosystem capable of supporting complex, cross-border transactions. London is firmly established as the largest Islamic finance centre outside the Muslim world.

Challenges facing Islamic finance in the UK

Misconceptions and narrow perception

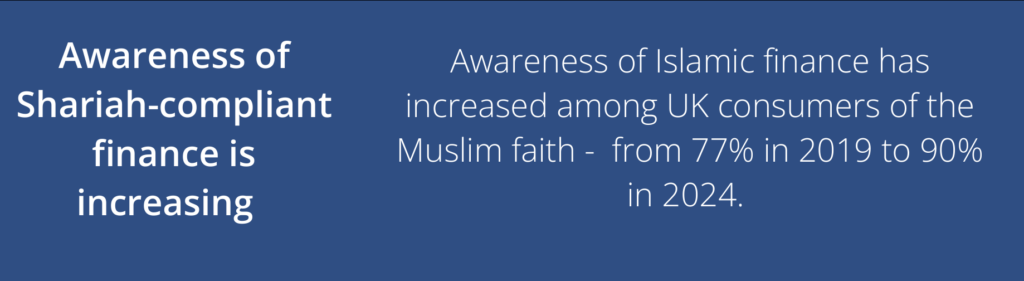

A lack of understanding remains one of the biggest hurdles facing Islamic finance in the UK. Research from Gatehouse Bank found that 24% of respondents (PDF) are unsure how Islamic finance works, with women in particular reporting lower familiarity with Sharia-compliant products (PDF). That gap in understanding means that Islamic finance can still be seen as complex, opaque or only relevant to a small group.

Findings from the UK Islamic Finance Council point to the same issue, highlighting the need for clearer communication around the ethical foundations of Islamic finance and its alignment with the UN Sustainable Development Goals. Against the mainstream UK market, these misconceptions can undermine confidence. They also feed a stubborn perception that Islamic finance is “only for Muslims”, narrowing appeal just as interest in ethical and ESG-aligned finance is widening.

Narrower product range and headline comparison

Islamic finance in the UK operates with a narrower range of products than the conventional system, a constraint regularly cited as a brake on broader adoption. Choice and flexibility are often taken as proof of value, so a narrower offer can invite short-sighted comparison with conventional alternatives.

The challenge comes when those comparisons fixate on headline price or availability, rather than structure, risk profile or long-term value. PR cannot change product design or pricing, but it can change how products are judged. Clear positioning, consistent language and proactive narrative framing help ensure that a product is understood for what it is, rather than a perceived weakness.

Cost sensitivity and value perception

Pricing remains a visible pressure point; a fifth of respondents of the Gatehouse Bank report cited higher fees or costs as the biggest deterrent to using Islamic finance products, while others expressed concern about potentially lower returns compared with conventional alternatives. Without clear narrative framing, these concerns can dominate external perception, even when ethical alignment or long-term value is a stronger differentiator.

Being judged by mainstream standards

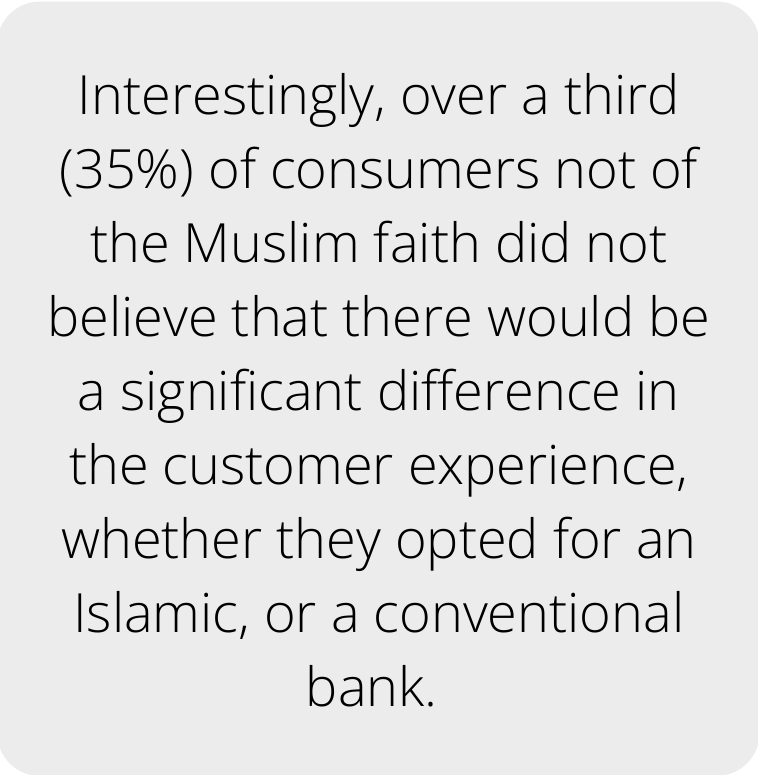

As Islamic finance moves into the UK mainstream, providers lose the protection of being seen as “different”. Gatehouse Bank’s research shows that 35% of non-Muslim consumers expect no meaningful difference between an Islamic and a conventional banking experience.

That expectation means Islamic finance providers need to compete head-to-head with mainstream institutions and face the same regulatory, reputational and media scrutiny. Vague explanations and assumed understanding won’t stand up. Providers have to be clear about what they offer, how they operate and why it matters, every time.

The opportunities this creates

These challenges open the door to opportunity. With the right communications strategy, providers can define how Islamic finance is understood and adopted.

Making relevance broader

-Across the UK, interest in ethical and green finance is growing which creates an opportunity for Islamic finance. PR can help connect Sharia-compliant finance to values such as transparency, ethical investment and long-term responsibility. PR can help frame Islamic finance in a way that resonates without diluting its credibility or oversimplifying what makes it different.

Winning the right comparisons

Price will always be part of the comparison but the opportunity lies in ensuring it isn’t the only one. Gatehouse’s research shows that trustworthiness and transparency are among the strongest motivators, particularly for non-Muslim consumers. Strategic communications helps make those qualities visible, so Islamic finance is judged on structure, governance and long-term value, not just on pricing.

Helping growth across demographics and regions

The report points to strong willingness to switch among younger audiences and clear generational differences in awareness and engagement. As activity expands beyond London into the UK regions, PR can support providers in engaging these new audiences through regional stakeholders and local media to ensure growth.

How PR and communications support Islamic finance providers in the UK

As Islamic finance becomes more visible, PR can bring a broad toolkit of disciplines which work together to help providers shape perception and support growth.

Media relations

Media relations helps Islamic finance service providers manage how they are covered by mainstream financial and business media. This includes shaping how products are described, ensuring context is included when comparisons are made with conventional finance and positioning organisations as credible participants in wider financial conversations.

Thought leadership and content

Thought leadership is one of the most effective tools in a PR strategy. For Islamic finance solution providers, it allows them to set the agenda and create conversations.

In practice, this includes developing commentary to explain strategic decisions, regulatory context and market trends. Thought leadership can help how Sharia-compliant structures operate, how governance and risk are handled and how providers see the UK market evolving. That clarity helps media, investors, banks, regulators, and stakeholders judge shariah-compliant financial services providers on its substance.

Digital communications and digital marketing

Digital communications isn’t just about having the right words on a website, but using those digital channels to build credibility, generate demand and support growth.

That means creating SEO-led content which answers the questions people are searching for about Islamic finance. It means using digital PR to earn authority through credible coverage and links. It means targeted campaigns which reach the right sectors or investor audiences, backed by data that shows what’s landing and what isn’t.

Social media

For Islamic finance providers, social media can help amplify coverage, reinforce key messages and extend thought leadership beyond traditional media. It can add clarity around announcements and market developments and gives organisations a direct way to engage with journalists and stakeholders. Social media should be deliberate with clear targeting and consistent messaging which aligns with wider PR activity.

Crisis communications and reputation management

Crisis readiness is about anticipating scrutiny rather than reacting to it. This includes identifying areas where misunderstanding could happen, stress-testing language and ensuring there is a clear response framework in place. This supports faster decision-making and reduces the risk of reputational damage caused by hesitation or inconsistency.

Islamic finance in the UK is growing and moving firmly into the mainstream. That visibility brings challenges, but it also creates opportunity. PR and strategic communications can give Islamic finance providers control over how they are understood and support growth in practical ways as the sector continues to evolve in the UK.

Do you want to learn how PR can support your growth in the UK Islamic finance sector?